CHCPE Income Limits for Connecticut Seniors in 2026

One of the first questions families ask when looking into home care support for a senior in Connecticut is whether they will even qualify financially. It is a fair question, and the answer is more accessible than most people expect.

What Is the CHCPE and Who Is It For?

The Connecticut Home Care Program for Elders, known as CHCPE, is a state and federally funded program administered by the Connecticut Department of Social Services. It is designed to help Connecticut residents aged 65 and older receive the support they need to continue living at home rather than moving into a nursing facility.

Services available through CHCPE include personal care assistance, home-delivered meals, homemaker support, adult day care, companion services, transportation, and emergency response systems, among others. Two of the most impactful options within the program are Adult Family Living, which allows a family member or close friend to become a paid live-in caregiver, and Personal Care Assistance, which brings a trained attendant into the home during approved hours.

To qualify, an applicant must be 65 or older, a Connecticut resident, and assessed as needing assistance with daily activities such as bathing, dressing, eating, toileting, or taking medications. Financial eligibility is the other side of that equation, and it is where many families get stuck.

Does CHCPE Have an Income Limit?

Yes, but not in the way most people assume. CHCPE has two funding pathways, a Medicaid funded option and a state-funded option, and each carries different income and asset rules. Understanding which pathway applies to a given situation determines whether someone qualifies and what their cost of participation looks like.

The key takeaway is this: even if someone’s income is above the Medicaid limit, there may still be a pathway to services through the state-funded tier or through a spend-down process guided by DSS.

CHCPE Income Limits: State-Funded vs Medicaid-Funded

Medicaid-Funded CHCPE

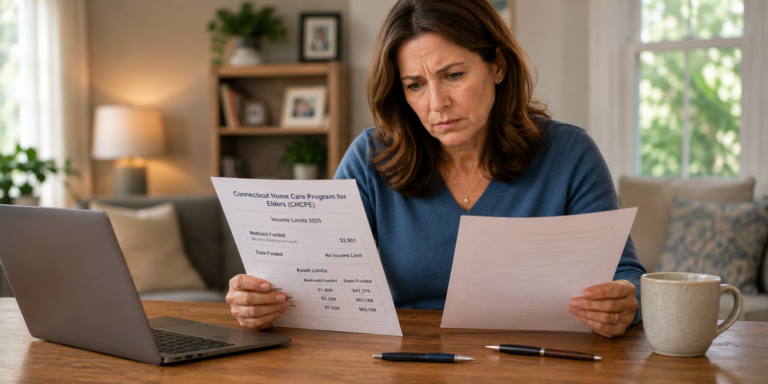

To qualify under the Medicaid waiver, a senior’s gross monthly income must be at or below $2,901.00 per month. This is the total income before any deductions, including deductions for Medicare premiums. Only the applicant’s own income is counted. For married applicants, a spouse’s income is not included in this calculation.

State-Funded CHCPE

The state-funded tier has no specific income limit. A senior whose income exceeds the Medicaid threshold may still qualify for services through this pathway. However, participation in the state-funded program is based on availability of funds, and state-funded clients are required to contribute 3% of the cost of their services.

This distinction is not always obvious. Many families assume that being over the Medicaid income limit means no access to the program at all. That is not the case.

What Counts as Income for CHCPE?

CHCPE looks at gross monthly income, meaning the total amount received before any deductions. This includes:

- Wages from employment

- Social Security benefits

- Pension income

- Veterans’ benefits

- Supplemental Security Income (SSI)

- Any other income received on a regular basis

Medicare premium deductions do not reduce the countable income figure. Only the applicant’s own income is assessed. If the applicant is married, their spouse’s income is counted separately and does not affect the applicant’s eligibility calculation.

CHCPE Asset Limits: What Else Affects Eligibility?

Income is only part of the financial picture. CHCPE also applies asset limits, and these differ depending on which funding pathway applies.

What is not counted as an asset:

- The applicant’s primary home

- Household furnishings and personal belongings such as clothing and jewelry

- The motor vehicle used as the primary means of transportation

- Irrevocable burial funds up to $10,000 per person

- Revocable burial funds up to $1,800

- Burial plots, including casket, outer container, and opening and closing of the grave

- Life insurance policies with a total face value of $1,500 or less (term life policies are excluded regardless of value)

What is counted as an asset:

- Bank and credit union accounts including savings, checking, CDs, IRAs, and vacation or Christmas club accounts

- Real estate not used as a primary residence

- Non-essential vehicles, campers, and boats

- Stocks, bonds, and US savings bonds

- Revocable trust funds

- Cash surrender value of life insurance where total face value exceeds $1,500

For jointly held assets, the full value is counted unless the applicant can demonstrate that another person, not a spouse, holds ownership.

Asset limits by funding type:

Medicaid-Funded State-Funded

Individual $1,600 $47,376

Couple (both receiving services) $3,200 $63,168

Couple (one receiving services) $1,600* $63,168

*A higher amount may be allowed if a spousal asset assessment is completed.

What If Your Income Is Over the CHCPE Limit?

Being over the Medicaid income limit does not automatically disqualify a senior from CHCPE services. There are established pathways that DSS can guide applicants through depending on their situation.

State-Funded Services

For seniors whose income exceeds $2,901 per month, the state-funded tier remains an option if assets fall within the state-funded limits. The trade-off is a 3% cost participation requirement and the fact that program availability depends on available funding.

Spend-Down Process

For some applicants whose income is above the Medicaid threshold, DSS can guide them through a spend-down process. This involves applying excess income toward qualifying medical expenses until the Medicaid income limit is met for that period. The spend-down is not automatic and is assessed on a case-by-case basis through DSS.

This is one of the most searched aspects of CHCPE eligibility and one of the least clearly explained on most informational pages. If a senior’s income is close to the limit, it is worth having a direct conversation with a qualified provider before assuming the program is out of reach.

CHCPE Eligibility Beyond Income: The Functional Requirements

Financial eligibility is only one part of qualifying for CHCPE. The program also requires that the applicant have a demonstrated functional need for assistance with daily activities.

Specifically, an applicant must need help with critical activities of daily living such as:

- Bathing and personal hygiene

- Dressing

- Eating

- Toileting

- Taking medications

- Mobility and transferring

This need is assessed through an in-home evaluation conducted by a care manager. The assessment determines not only whether the applicant qualifies but also the level of care required, which shapes the services they receive and, in the case of AFL, the caregiver’s stipend level.

Age and residency requirements also apply. The applicant must be 65 years of age or older and a legal Connecticut resident.

Navigating the CHCPE Application from Start to Finish

Understanding the income and asset limits is a strong starting point, but navigating the full CHCPE application process, including Medicaid enrollment, functional assessments, program selection, and DSS coordination, involves more steps than most families expect.

Gifted Hands Homecare is a DSS-authorized provider in Connecticut. We help seniors and their families determine eligibility, work through the application process, and get enrolled in the right program, whether that is Adult Family Living or Personal Care Assistance. There is no cost to the family for our support.